The New-Home Market Isn’t Collapsing. But Prices Are Losing Support.

New home sales fell in April, another sign that deteriorating household financial conditions are cooling housing demand. The rise in new home inventory sets up future price declines.

New home sales fell in April, another sign that deteriorating household financial conditions are cooling housing demand.

Sales were 11.3% lower than a year ago, and the April pace was the slowest for any April since 2022 — the last time mortgage rates rose sharply enough to quickly reset the market. Mortgage rates reached a nine-month high in April as geopolitical risks and other factors pushed Treasury yields higher. I wrote more about that in my Treasury yield decomposition here: https://www.orphedivounguy.com/treasury-yield-decomposition/

But mortgage rates are still below year-ago levels. That means rates are not the whole story.

The bigger issue is that household balance sheets are under pressure. Hiring rates, quits and job switching remain low, while real disposable income has been falling for three consecutive months. Consumers are drawing down savings and relying on credit to smooth consumption. I discussed that pressure in my April Personal Consumption Expenditures report reaction here: https://www.orphedivounguy.com/april-2026-pce-report/

At the same time, credit balances continue to rise and debt-to-income ratios are moving higher. That matters directly for housing because the most common reasons borrowers are denied a mortgage is an elevated debt-to-income ratio.

The result is a market where new-home demand remains soft relative to supply.

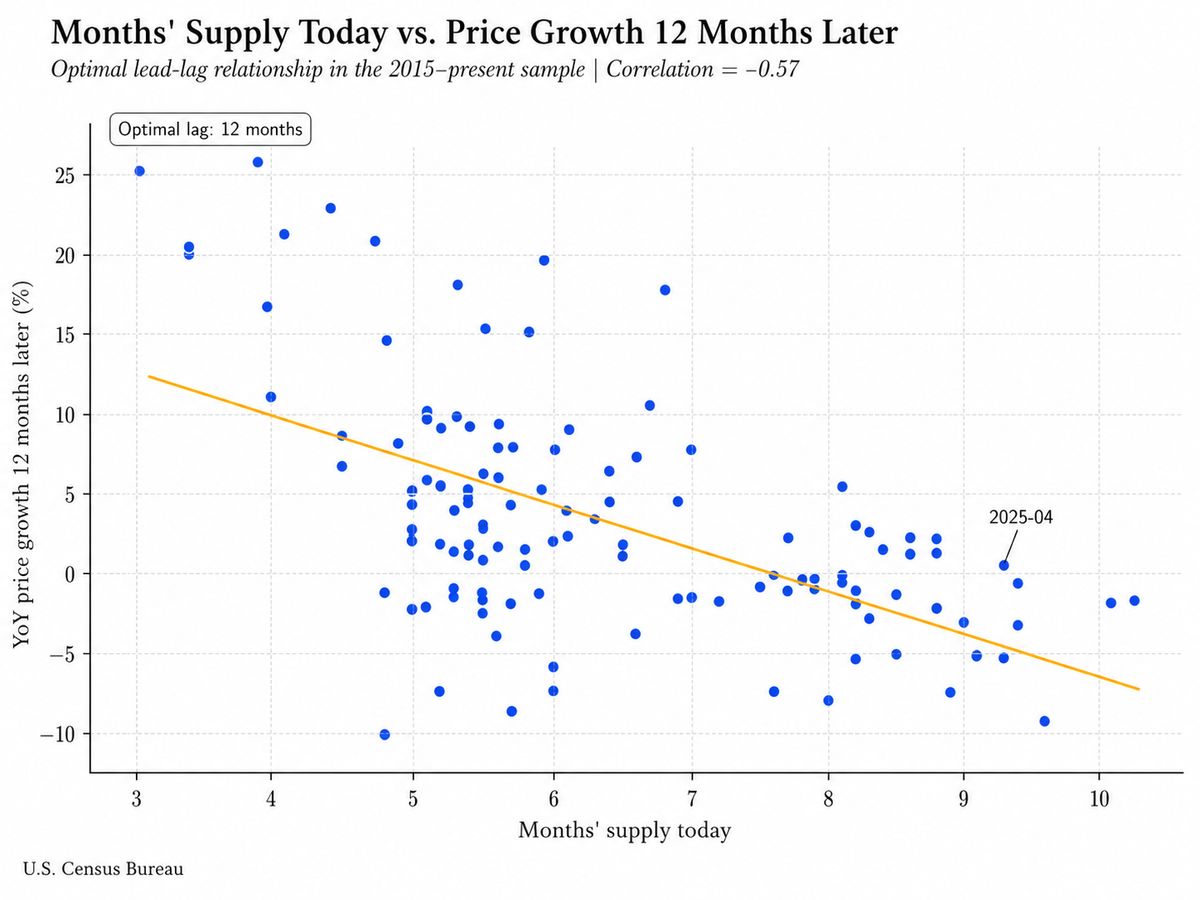

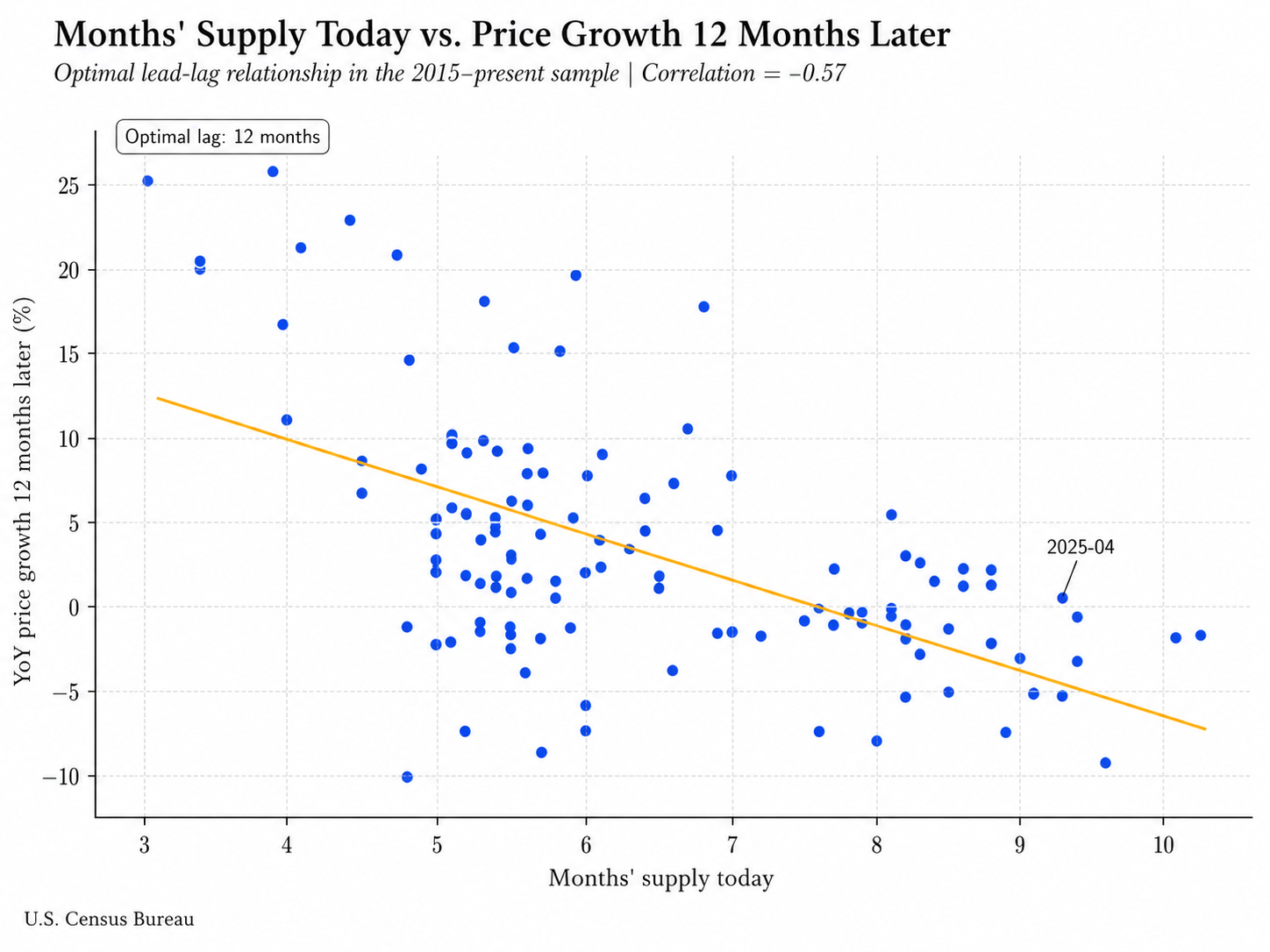

That shows up clearly in months’ supply, one of the best measures of market balance. Months’ supply tells us how long it would take to sell the current inventory of new homes at the current sales pace. It combines both sides of the market: how many homes are available and how quickly buyers are absorbing them.

Months’ supply rose to 9.4 months in April, up from 8.6 months a year ago.

That increase does not mean builders are flooding the market with homes. In fact, completions have been slowing rapidly. The rise in months’ supply mostly reflects a sluggish sales pace. When demand weakens, homes sit longer, and months’ supply rises.

And that matters for prices.

Historically, higher months’ supply has been associated with weaker price growth later on. In the data since 2015, the relationship is strongest at about a 12-month lag: elevated months’ supply today tends to be followed by softer year-over-year price growth roughly one year later.

Prices do not have to fall immediately just because inventory rises. But when homes sit longer and supply builds relative to demand, builders usually respond with price cuts, incentives, mortgage-rate buydowns or a slower pace of new starts.

The new-home market is not collapsing. But it is becoming less tight. Slower sales today are setting the stage for softer prices tomorrow.