June 2026 FOMC Meeting: No Cut, No Hike And What the Taylor Rule Says About the Fed's Hold

Key Takeaways

- The Fed held at 3.50%–3.75% in June, at Kevin Warsh's first meeting. It trimmed the statement and dropped the easing bias, and the dot plot moved from a cut bias to a slight hiking bias.

- Unemployment is 4.3%, right on the Fed's 4.2% long-run estimate. There is little evidence of labor-market slack in the Fed’s own projections to justify a cut.

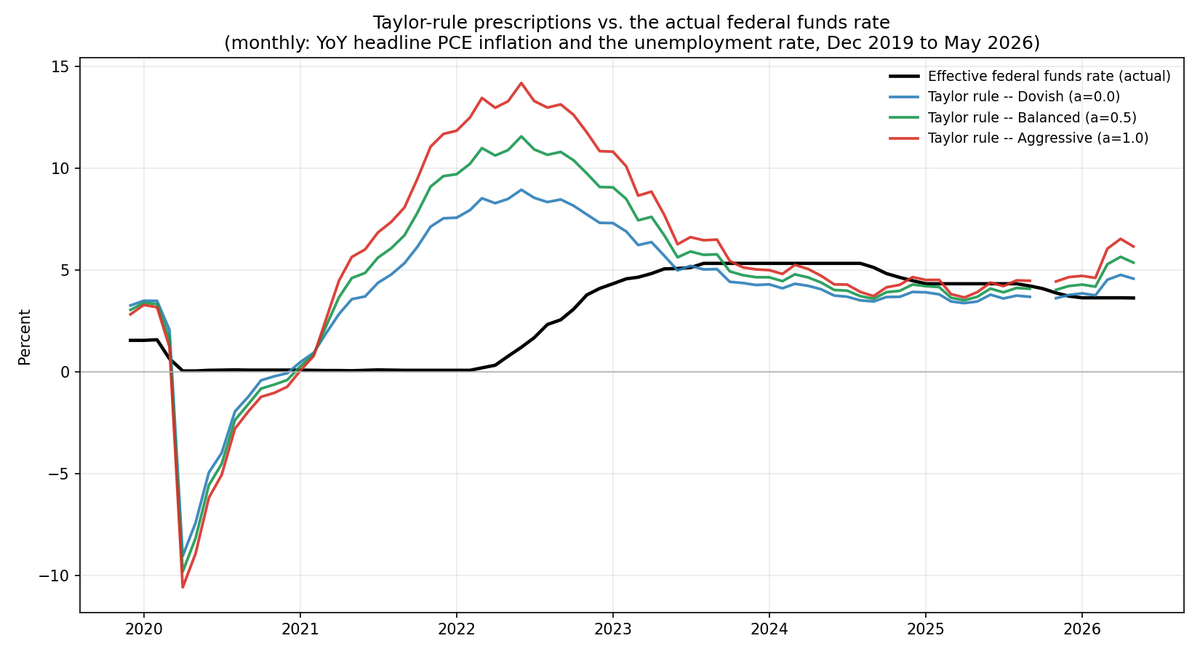

- Feed current inflation — 3.8% headline PCE through April (BEA) — a balanced Taylor rule prescribes about 5.7%, above today's rate. On the Fed's own year-end projections it prescribes about 5.4%, roughly 1.6 points above the 3.8% median dot.

- That dot is consistent with the rule only if inflation falls to about 2.5%. The Fed's 2027 projection (2.3% PCE) says it expects that. I think it's right: the energy shock is a one-time shift in the price level — a tax on households and firms — that fades unless it leaks into wages and expectations.

The Fed held the line in June. No cut, no hike — and no promise that relief is coming soon.

That was the right call. The Taylor rule shows why a cut wasn't justified, and why the Fed's own projections only hold together if it expects today's inflation to fade. I think it will.

What changed in June

Three things. The statement got shorter — about 115 words, down from over 300 — and the easing-bias line that had signaled a coming cut was gone. The median 2026 dot rose to 3.8% from 3.4% in March; 9 of 18 participants put their year-end dot above the current rate, 8 held, 1 cut (FOMC SEP, June 2026). And the inflation forecast jumped: year-end PCE to 3.6% from 2.7%, core to 3.3%.

None of that is a commitment to hike. It's the removal of a commitment to ease.

Taylor rules out a cut

The Taylor rule sets a policy rate from a neutral rate plus two terms: one for inflation's distance from 2%, one for the economy's distance from full employment. Both terms matter. Right now only one is doing any work.

Unemployment is 4.3%, essentially the Fed's 4.2% long-run estimate (FOMC SEP), so there is no slack. Payrolls grew 172,000 in May (BLS). The employment term is therefore close to zero, and inflation sets the result — 3.8% headline PCE through April, 3.3% core (BEA). It points up.

How far up depends on how hard the rule leans on inflation. Three standard weightings, all anchored to the Fed's 3.1% longer-run dot as the neutral rate:

| Taylor-rule scenario | Inflation fed in | Prescribed rate |

|---|---|---|

| Aggressive (strong inflation response) | 3.8% (current) | 6.6% |

| Balanced — Taylor (1993) | 3.8% (current) | 5.7% |

| Dovish (muted inflation response) | 3.8% (current) | 4.8% |

| Balanced, on the Fed's own year-end PCE | 3.6% | 5.4% |

| Balanced, on the Fed's 2027 (post-shock) view | 2.3% | 3.5% |

| Memo: current target midpoint | — | 3.6% |

| Memo: Fed's median 2026 dot | — | 3.8% |

Every column on current inflation sits above today's 3.6%. The rule says the Fed is, if anything, slightly too easy. Under the Taylor-rule specifications shown here, there is no case for a cut.

The dots already price disinflation

Feed the rule the Fed's own year-end projections — 3.6% PCE, 4.3% unemployment — and it prescribes 5.4%. The Fed's median dot is 3.8%. That is a 1.6-point gap between the rule and the committee's own rate path.

Invert it. At 4.3% unemployment, the 3.8% dot squares with this rule only if inflation is about 2.5%, not 3.6%. The rest of the projection agrees: the 2027 PCE dot is 2.3% (FOMC SEP). Feed that in and the rule lands at 3.5% — the dot.

So the hold is a forward-looking rule, reacting to where inflation is going rather than where it is. The gap between the mechanical prescription and the dot is the disinflation the Fed is counting on.

An energy shock is a tax

That counts on a distinction worth keeping straight: the price level versus the inflation rate. An energy shock raises the level of prices once. It lifts year-over-year inflation now, because prices sit above last year's — but a one-time jump doesn't repeat. A year on, it sits in the base, and the rate falls back. The exception is if it feeds wages and expectations.

An oil shock also drains real income from households and firms and routes it to producers. It works like a tax, cooling demand for everything else. You don't meet that with rate hikes.

The horizon is the catch. One-year expected inflation was elevated in May, at about 3.5% in the Cleveland Fed model, though the June reading fell closer to 3.0%. Two-year expected inflation is lower, around 2.75%, and the Fed’s 2027 PCE projection is 2.3%. How far you look through the shock is the judgment call. Longer-run expectations have not broken loose — yellow, not red — and markets are not pricing a 1970s regime.

What this does and doesn't mean

The Taylor rule is a benchmark, not a mandate, and the inputs are uncertain. The neutral rate isn't observable; I tie it to the Fed's 3.1% longer-run dot, but plausible estimates span a point, and that moves every number in the table. The response weights are a choice, which is why I show a range. The unemployment gap is a noisy read on slack.

The look-through is conditional. It holds only while the shock stays a relative-price move. If it feeds wages and medium-term expectations, the framing breaks and the case for a hike becomes real. That is the contingency to watch.

What holds up is narrower. Across the specifications shown here, the labor market gives no reason to cut, and current inflation puts the prescription above today's rate. The Fed's dot is reconcilable with this Taylor-rule specification only under an explicit disinflation assumption — and the Fed does not bind itself to any single rule. The decision to wait follows from those two facts.

Bottom line

The hold is consistent with the mandate. Full employment plus above-target inflation rules out a cut and, on current inflation, leans toward tightening. The Fed isn't tightening because it is betting the energy shock fades — a bet visible in its own projections, where the rate path only works if inflation falls toward 2.5% and then to target.

Cutting before inflation begins to move lower would tell households and firms the Fed will blink first — and that is how a one-time price shock turns into a persistent one. Relief may come later this year if inflation eases, as I expect. The Fed just can't act on it yet.

Methodology

The prescribed nominal rate is i* = r* + π + a·(π − π*) + b·[ −φ·(u − u*) ], with π the inflation input, π* = 2.0%, u the unemployment rate, u* = 4.2% (the median June 2026 SEP longer-run projection), and φ = 2 (Okun). The leading "+ π" is the Fisher term, so the total inflation response is (1 + a). The three variants vary only the inflation-gap weight a, holding the output-gap weight b = 0.5: dovish (a = 0.0), balanced (a = 0.5, Taylor 1993), aggressive (a = 1.0).

The neutral real rate is r* = 1.1%, backed out of the Fed's June 2026 longer-run funds dot (3.1%) minus the 2% target, so the rule stays internally consistent with the SEP. The "rule-consistent inflation" inverts the balanced rule for the inflation rate that sets i* to the 3.8% median 2026 dot at u = 4.3%; the solution is 2.53%. The forward-looking prescription feeds the rule the Fed's 2027 median PCE projection (2.3%). Near-term expected inflation is the Cleveland Fed's one-year model-based series (CPI basis; a ~0.3pp wedge applies versus PCE).

Federal funds rate, PCE and core PCE (year-over-year), and unemployment are from FRED; projections and dots are from the FOMC SEP, June 17, 2026; CPI and payrolls are May 2026 from BLS. The rule's prescriptions are sensitive to r*, the weights, and the unemployment-gap proxy, and the forward-looking reading is conditional on expectations staying anchored.

Sources: Federal Reserve, FOMC statement and Summary of Economic Projections (June 17, 2026); U.S. Bureau of Economic Analysis (PCE price index); U.S. Bureau of Labor Statistics (CPI, Employment Situation, May 2026); Federal Reserve Bank of Cleveland (model-based inflation expectations); Federal Reserve Bank of St. Louis (FRED).